While the unbridled rise of guest room rates may be slowing from the Great Recession recovery period of the last few years, the question of when the current cycle may actually conclude and another begin is unanswered. Results from our annual Meetings Today Trends Survey point to a gradual equilibrium in the market, with attendance and the number of meetings rising, along with a slightly less-pessimistic view regarding budgets.

“You're starting to hear people on the hotel side ask if we're near the end of the cycle,” says Bobby Bowers, senior vice president of operations for STR, which tracks U.S. hotel trends. "This will be the fifth consecutive year of RevPAR [Revenue Per Available Room, a key performance metric in the hotel industry] growth and the last cycle was a five-year cycle, and the one before that was a nine-year cycle.

“I don't think that we're there yet, but when you hear people start to talk about the end of a cycle, it's definitely on their minds," he continues. "Unless you have an event or something that goes on with the economy—some type of a shock that we don't expect.”

As the Great Recession Recovery days of sharply rising guest room rates are starting to cool, it seems the market has stabilized, with supply and demand reaching equilibrium, although supply is still ticking up in some key destinations.

“Right now, the trends seem to say we're on a pretty steady path,” Bowers says. “But from the lodging industry perspective, I don't think you're going to see RevPAR growth as high as it's been the last few years.”

In a general sense, times are good for hoteliers, who face the "high-class problem" of a robust market that is finally hitting a ceiling and doesn't have much room to grow.

In a general sense, times are good for hoteliers, who face the "high-class problem" of a robust market that is finally hitting a ceiling and doesn't have much room to grow.

“I think what you're seeing, in the macro sense, is a little bit of an increase in the room supply—not huge, but a pretty steady upward climb,” Bowers says. “On the demand side of things, there's sort of a slowing of growth. We're seeing continued growth, but just at a lot slower pace. What's starting to happen is RevPAR growth is starting to decline, but you've still got enough occupancy traction that you're not seeing a decline in rates across the board.”

Bowers expects that hotel room prices will finish the year up, in the 4 percent to 6 percent range, with the upper end of the chain scale—which is experiencing healthy occupancy rates—enjoying the most growth.

“I think we'll see that as we move into 2016, a growth rate of 5 percent or so, but slower occupancy growth,” he says of the overall U.S. lodging market.

Bowers points out that about 10 percent of hotel rooms under construction are in New York City, which has about 13,500 rooms in the pipeline and is experiencing a high occupancy rate that shows no sign of slowing.

“The number-two market is Houston, and what's under construction in New York is over twice as many rooms as the second-highest market," Bowers explains. "A lot of new room supply is coming on-line there.”

Houston, however, is seeing demand drop as a result of the lagging oil market.

“In the shorter term they're going to face some challenges because supply is growing and demand is decreasing," Bowers says. "That's a temporary thing because the price of oil will go up, but right now they're in the lurch.”

Dallas is also seeing an increase in rooms under construction, Bowers added, and "shared-economy" supply from companies such as Airbnb are starting to slow down the growth rate significantly.

Value markets continue to be major Midwestern and nearby destinations—anything away from the coasts. Nashville, Tenn., with its new convention center, should be a particularly hot market with relatively low rates in the near-term, Bowers contends, with perennial convention favorite Orlando also continuing to offer agreeable rates.

According to Bowers, the recent Federal Reserve decision to raise interest rates should have a minimal effect on what is currently a steadily improving, healthy U.S. economy.

“These guys have been talking about an increase in rates for so long that I think the market has planned for that and baked it into the stock prices, so I don't think you're going to see a big shock with that," he says. "Overall, the economy's in pretty good shape, so you're looking at a 2016 that should look a lot like 2015, but just a little slower on the occupancy side of things, because in many markets it's so high that it's hard to move it.”

The Survey Results

The Survey Results

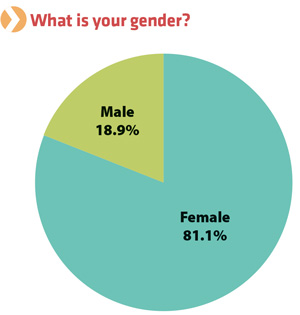

This year’s Meetings Today Trends Survey attracted complete responses from more than 600 meeting planners.

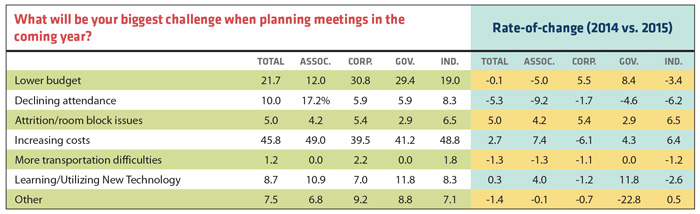

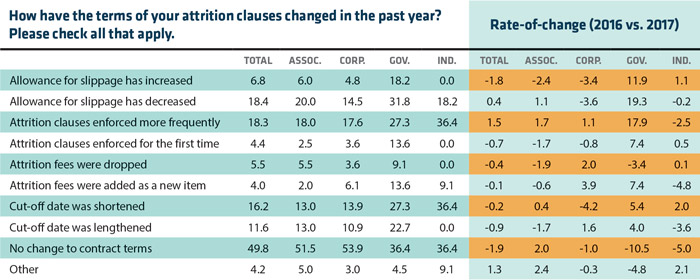

When asked what their biggest challenge in the next 12 months will be, lower budgets and increasing costs were the biggest trending items, although budget woes have subsided for association planners, especially from the survey conducted in 2014. Attrition terms also figured heavily into planners' top concerns, across all planning segments, next year.

Compared to last year’s survey, 5 percent more planners, overall, responded that attrition and room block issues would be their top concern, led by corporate planners (5.4% more) and association planners (4.2% more).

Lower budgets were the chief concern of 5.5 percent less corporate planners and 8.4 percent more government planners this year; 5 percent less association planners think their biggest challenge will be lower budgets in the 12 months following the survey.

Attendance is not expected to be a major concern next year, however, with 5.3 percent less planners, overall, listing it as their biggest challenge (9.2% less association planners, 1.7% less corporate; 4.6% less government planners; 6.2% less, independent).

Increasing costs were listed as the top challenge in the next 12 months by 49 percent of association planners, 39.5 percent of corporate planners, 41.2 percent of government planners, and 48.8 percent of independent planners.

On the trending side, when comparing this year’s results to last year’s, increasing costs were noted by 2.7 percent more planners, overall, as being their chief concern in the next 12 months, led by 7.4 percent more association planners; 6.1 percent less corporate planners, when compared to last year’s survey, cited increasing prices as their chief concern.

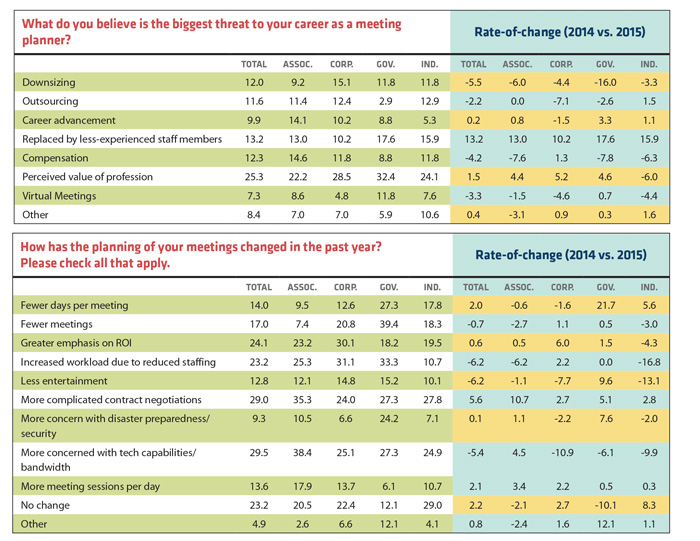

Threat Levels

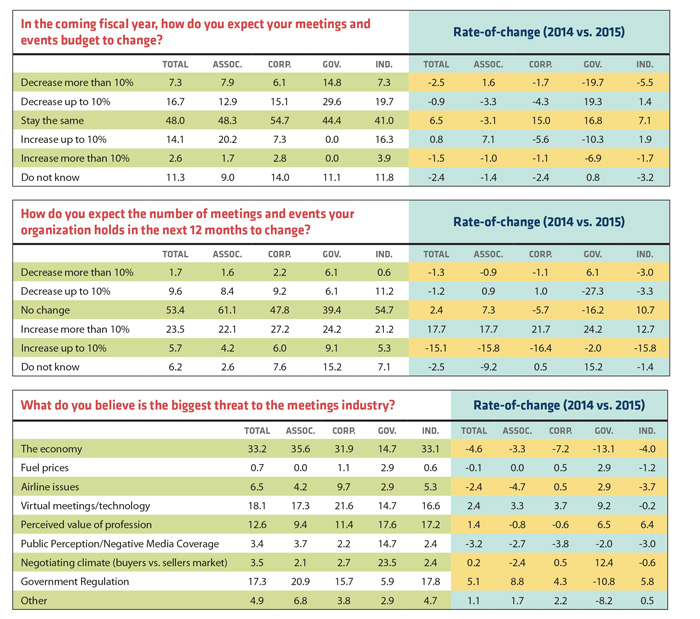

The economy was listed as the biggest potential threat to the meetings industry next year, with 33.2 percent of planners, across all segments, selecting that response option.

On a positive note, however, the number of respondents selecting the economy as the biggest threat to the meetings industry is on the decline, with 4.6 percent less planners overall selecting this option in this year's survey. This was led by 13 percent less government planners and 7.2 percent less corporate planners.

PageBreak

Virtual meetings were noted by 18.1 percent of planners as the biggest threat to the meetings industry, followed by government regulations, at17.3 percent, and the perceived value of the profession, by 12.6 percent.

Interestingly enough, concern about a bad negotiating climate was actually relatively low overall, to the point of being near the bottom of the list. Government planners were a huge exception here, though, with a whopping 23.5 percent listing it as their chief worry, a number that increased 12.4 percent from the previous survey, conducted at the end of 2014.

When it comes to where the rubber really hits the road with respondents, 25.3 percent, overall, listed the perceived value of their profession as their chief concern from a career standpoint, reflecting that the stubborn problem of the value of the profession is still top-of-mind, despite years of industry association work to increase the clout of meeting planning positions. This response option was followed by “replaced by less-experienced staff members” (13.2%), compensation (12.3%), downsizing (12%) and outsourcing (11.6%).

The “replaced by less-experienced staff members” option saw a large increase in this year’s survey, with 13.2 percent more planners selecting it in this year’s survey when compared to the 2014 survey; 17.6 percent more government planners and 15.9 percent more independent planners are looking over their shoulder this year as compared to last.

Budgets

Budgets remained relatively flat over the last year, with 46 percent of all planners saying there were no changes, and an equal 18.8 percent saying it either increased or decreased by 10 percent.

Association planners responded that their budgets increased slightly, with 22.1 percent noting an increase of up to 10 percent, but government planners continue to have to work with less, with 38.2 percent saying their budget decreased up to 10 percent; 5.3 percent more corporate planners said their budget decreased up to 10 percent in this survey when compared to the 2014 survey.

Budget expectations for 2016 are similarly conservative, with nearly half of the overall respondents expecting their budget to remain flat when compared to 2015.

Association planners were a little more optimistic, however, with 20.2 percent believing their budget will increase up to 10 percent, and 15.1 percent of corporate planners expect a decrease of up to 10 percent. No government planners thought their budget would increase at all, with nearly 29.6 percent believing their budget would be cut up to 10 percent and almost 15 percent responding that their budget could be slashed more than 10 percent.

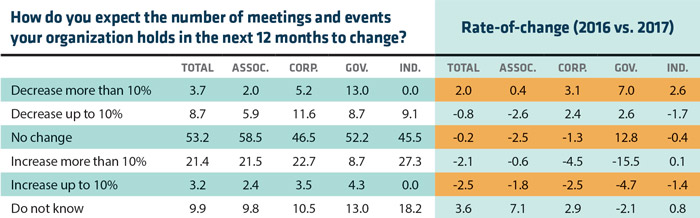

Number of Meetings/Attendance

The number of meetings held in 2016, in general, is expected to increase, with 23.5 percent of planners expecting an increase of up to 10 percent; 53.4 percent say they think their attendance numbers will remain flat next year.

The rate-of-change is on the upswing, however, with 17.7 percent more planners overall expecting their number of meetings to increase up to 10 percent.

The outlook for attendance seems very healthy, with 23.5 percent of respondents overall expecting an increase of up to 10 percent, and 5.7 percent think their attendance will increase more than 10 percent. A very healthy 22.1 percent of association planners predict their attendance will increase up to 10 percent, along with 27.2 percent of their corporate counterparts, 24.2 percent of government planners and 21.2 percent of independents.

The rate of change between the survey conducted at the end of 2014 and the 2015 poll found 17.7 percent more association planners believing their attendance will rise by up to 10 percent, along with 21.7 percent more, corporate, 24.2 percent more, government and 12.7 percent more, independent.

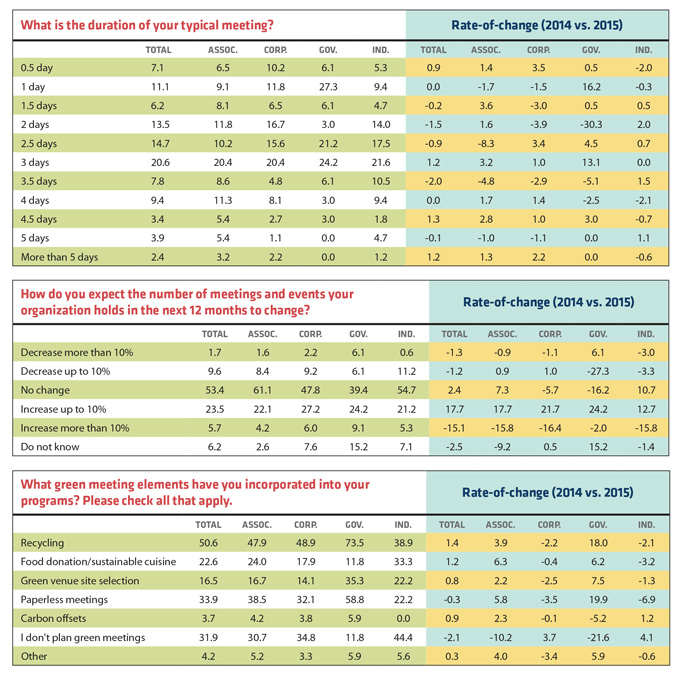

Duration of Meetings/Planning Cycles

Duration of Meetings/Planning Cycles

The average length of a meeting came in at three days, across all segments except for government planners (27.3% said 1 day, although 21.2 percent noted 2.5 days and 24.2% responded 3 days). The rate of change between the 2014 and 2015 surveys was relatively flat.

A short booking window seems to have become the new normal, with 72.3 percent of planners, overall, noting that they expect their planning cycle to be about the same as last year, with 17 percent believing it will be shorter and 10.7 percent expecting their cycle between booking facilities and the actual occurrence of their events to be longer. From 2014 to the 2015 survey, 12.7 percent more government planners think their booking window will decrease. Association, corporate and planner rates of change were fairly flat, reflecting a status quo may be setting in.

Videoconferencing/Hybrid Meetings

Although not dramatic, non-face-to-face meetings are creeping into the meetings equation, with 28.5 percent of planners, overall, saying they are replacing up to 25 percent of their meetings with videoconferencing, although 61.9 percent said they are replacing no meetings at all. The number of planners replacing up to a quarter of their meetings with videoconferencing was skewed heavily by government planners, of which 54.5 percent said up to 25 percent of their face-to-face events will be replaced.

Trend-wise, 10.5 percent more planners this year said videoconferencing replaced up to 25 percent of their meetings, led by 37.9 percent more government planners. A little more than 20 percent of association planners said videoconferencing will replace up to a quarter of their meetings, while 30.5 percent of corporate planners noted the same.

Hybrid meetings, which mix face-to-face with a virtual component, were still a bit of a rare bird, with 6 percent overall responding that they held a hybrid event last year; the rate of change was relatively flat between the last two surveys.

Green Meetings/CSR

The number of planners expecting to plan a green meeting next year is relatively unchanged from the 2014 survey, with 37.8 percent responding yes and 62.2 percent answering no. Nearly 4 percent more association planners noted they expected to hold a green meeting next year, and government planners were up 4.1 percent in this category.

Corporate planners were lagging, however, as a sizable 8.5 percent less think they'll plan a green meeting in the 12 months following the survey.

Corporate social responsibility, or CSR, seems to be in a growth mode, with 4.1 percent more of planners, as a whole, responding that they expect to include a CSR program in their meetings and events.

The Big Picture

The meetings industry seems to have plateaued, with attendance expected to rise and the growth in hotel room rates increasing as a slower pace than in the last few years. Meeting planners did express acute concern with an overall rise in the costs associated with their meetings, although the outlook on the strength of their budgets was not decidedly pessimistic.

While wild cards such as the strength of the economy, the Federal Reserve’s decision to increase interest rates (although just by half a percentage point initially) and uncertainties about terrorism attacks at home and abroad may crop up to roil the waters, the prognosis for the short-term seems to be stability and a healthy outlook as we head into 2016.

The 2016 Meetings Today Trends Survey is a proprietary Meetings Today online study that was distributed to 33,644 Meetings Today subscribers. As an incentive to complete the survey, respondents were offered a chance to win one of five $50 Visa gift cards.

Conducted from September to October 2015, the survey generated 604 complete responses.

Don't miss out on our 2016 Trends and Strategies video broadcast, live from PCMA's Convening Leaders.